locking variable to fixed rate

Is now the time?

With these changing times and growing uncertainty we would like to address the option of locking variable to fixed rate.

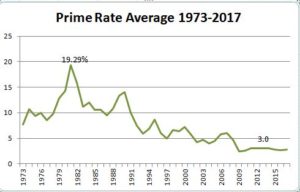

Historically the variable rate has been consistently more attractive than the fixed rate and the prime rate has remained constant.

Generally we have experienced prime rate changes in increments of no more than .25%, the next scheduled rate decision is December 6th.

One great option you have is the option to renegotiate and take advantage of locking variable to fixed rate.

to lock or not

As a variable rate mortgage holder you must be comfortable with the possibility of rate increases; have the income to cover potential increase in monthly payments, and continue to manage your existing debt. However, if you have a higher variable rate, it may be worthwhile to renegotiate your rate by locking variable to fixed rate and potentially extend your term.

If you find yourself losing sleep worrying about how you might meet your next mortgage payment if rates do increase, then it may be beneficial for you to lock into a fixed rate. One of the pros of the fixed rate is having a consistent monthly payment for the term of the mortgage.

stop the bus

Before converting to a fixed rate there are a few points to consider:

- Are you considering a move before your term is up? One key difference between variable and fixed is prepayment penalties. With a variable rate mortgage you are looking at 3 months interest to break the mortgage. On a fixed rate mortgage the prepayment penalty is the greater of, 3 months interest or interest rate differential (IRD). IRD is a lender calculation, which may be considerably higher. Our post, Breaking Your Mortgage will give you an idea of the numbers.

- Compare the payments. Depending on the remaining term, and long range speculation you may find savings by remaining variable. By comparing payments at both the variable and fixed rate you’ll have an idea of savings and or costs over the term.

next steps

It’s a big step making a change to your existing mortgage. We are happy to discuss your current financial situation and run some numbers, showing what the different scenarios may look like. After considering your options, comparing payments and forecasting, if you decide locking variable to fixed rate is the way to go, here’s what we suggest:

- Contact us! We will review your mortgage details and help you determine your next steps. Lenders will typically offer you their current posted fixed rate, we’ll help ensure you obtain the lowest fixed rate

- You will be offered a term equal to or greater than your current remaining term

- This is typically a quick process and the change will be implemented as soon as possible

Need some advice making the decision to lock in from variable to fixed? Call today, we’re happy to help.